Tsunami’s are primarily caused when an earthquake happens in the ocean. They can also be caused by landslides, meteors, storms, etc. They are unexpected, difficult to predict and the consequences can be catastrophic.

Carrier cost of insurance (COI) increases don’t take human life; however, they are unexpected, difficult to predict and their consequences on permanent life insurance can be devastating. Fortunately, like earthquakes in the ocean they don’t happen very often. They ARE occuring with more frequency now. We currently have 10 carriers (and counting) who have increased COI’s. It’s a real problem, pay attention!

Here are some of the examples cited by a top carrier for COI increases:

- updated mortality assumptions

- lower investment earnings

- updated expenses

- updated persistency/lapse assumptions

Let’s look at these more closely…

People are living longer and mortality is decreasing. That should be a good thing right? Live longer, pay more premiums. Every illustration I see with IRR numbers show lower IRR on cash value and death benefit the older the policy is which should be good for the company. However, lower investment earnings are really hurting carriers. We need interest rates to increase. General accounts of carriers are heavily vested with investment grade bonds. Average maturities are @10 years, the yield curve has been declining for decades and is just now starting to turn. Bond portfolios don’t turn around overnight so it could be several years before portfolio yields increase.

Carries have been becoming more efficient and “smaller” for quite some time now. Expense initiatives are everywhere. Ask anyone in distribution. It is expensive to distribute product so most carriers have reduced the size of their distribution teams. These expense initiatives don’t stop at distribution, they are company-wide. So it seems to me carriers are becoming leaner and more efficient which should be a good thing for policyholders. If people are living longer then the carrier lapse assumptions are inaccurate. Carriers need a percentage of their policies to lapse. It is built into the pricing. If people are living longer more policies will have claims that are not built into the pricing assumptions. Hedge Fund owned life insurance has reduced the number of policies carriers had expected to lapse.

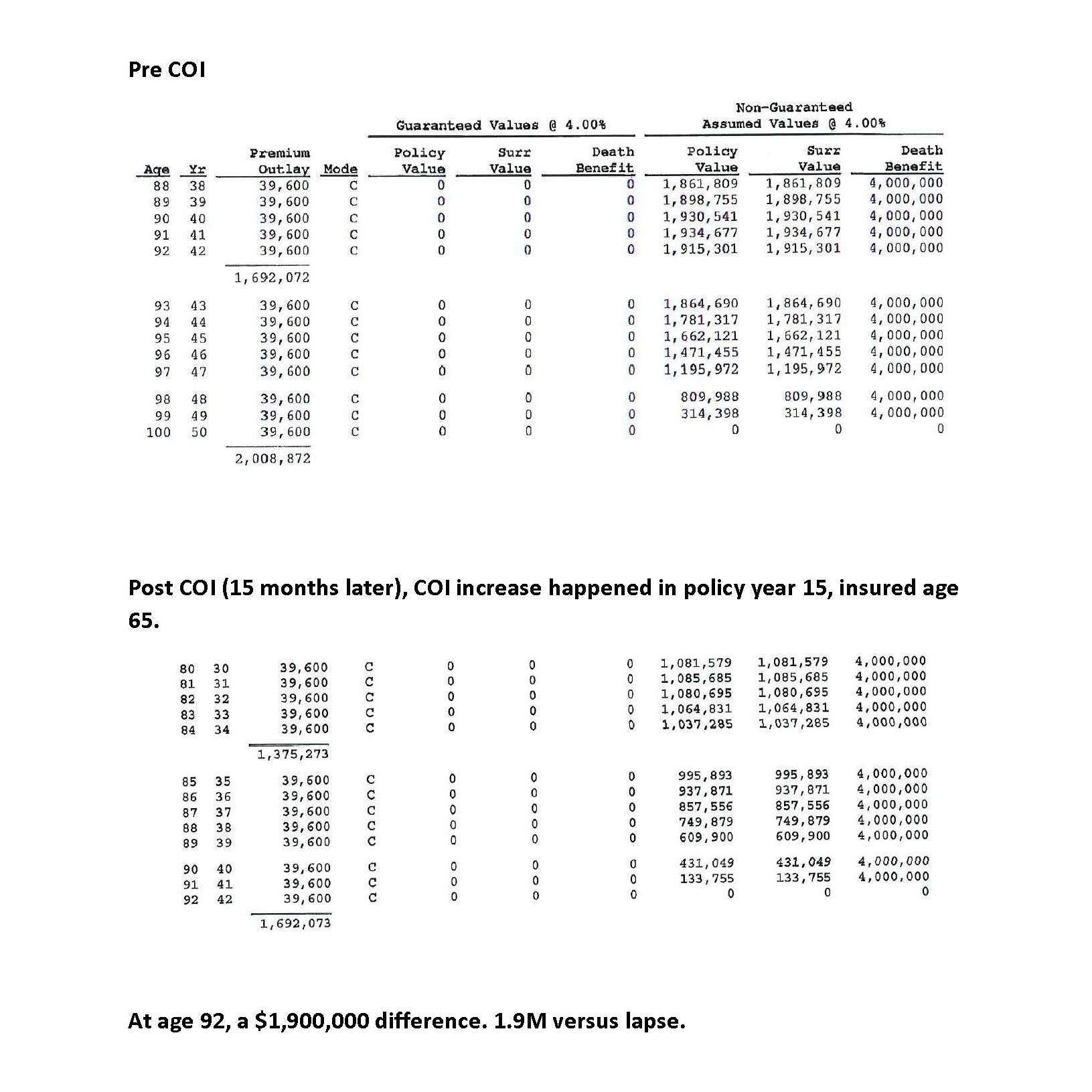

To see the effect COI changes have on a policy click here….

What does this mean for you? POLICY REVIEWS are critical!! Don’t stand by and let your client lose their policy because of a COI increase. Now is not the time to hide under the desk. You, the agent did not cause the crisis, it just happened. How you react and help your client with this urgent issue is how you will be judged by your clients. Performing a policy review will either assure your client they don’t have a problem or identify a problem and give you an opportunity to fix it. A renown industry speaker; Joe Jordan famously said, “never waste a crisis”. This is your opportunity to get ahead of the COI Tsunami crisis.

We can help. At The ASA Group we have a dedicated policy audit department which has a streamlined process for assisting producers with policy audits. This is a great opportunity for ASA to be a value add to your practice and for you to be a value add to your clients.

{kind=link}